Research has proven that working with a financial advisor to meet your retirement goals provides significant monetary value. In fact, Vanguard studies have shown that those who utilize a financial advisor see an approximately 3.0% additional increase in their net portfolio returns over time.

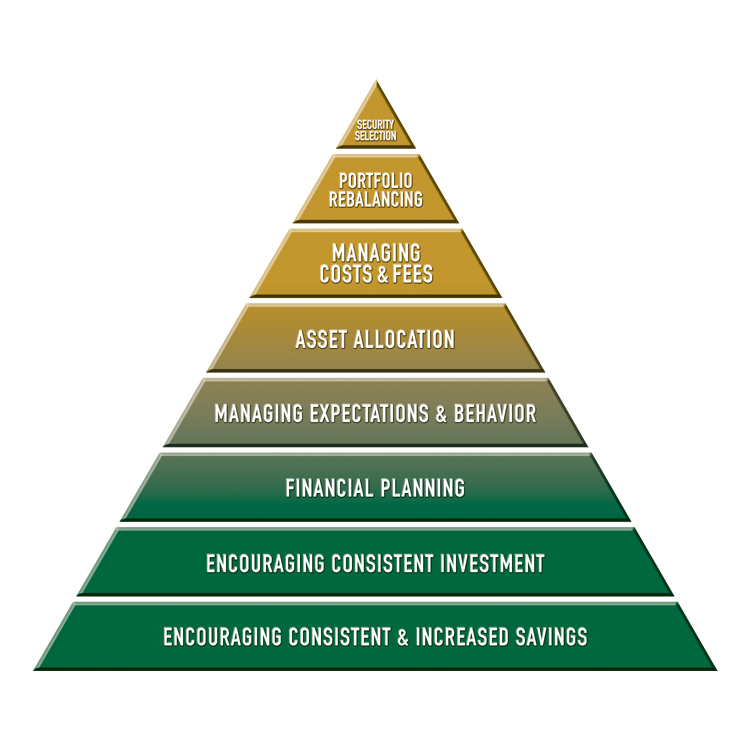

While many think stock selection is the primary driver of these returns, an advisor’s true value manifests itself in a variety of technical and non-technical ways. In other words, a good financial advisor not only helps you select the right stocks and avoid unnecessary risks, he or she also helps guide your behavior as markets fluctuate, ensuring you adhere to a wise financial plan. The true value of an advisor can best be summarized by a hierarchy of services provided to an investor.

Encouraging consistent and increased savings

Encouraging consistent and increased savings

A financial advisor’s role is to help clients understand how consistently saving money is the most important aspect of their financial wealth and health in the future. When it comes to how bright your future is, a good advisor will tell you that your savings rate is far more important than your rate of return. Good planning starts with getting a client’s financial house in order and ensuring a savings plan is in place with the proceeds invested into a solid, diversified portfolio.

Encouraging consistent investment

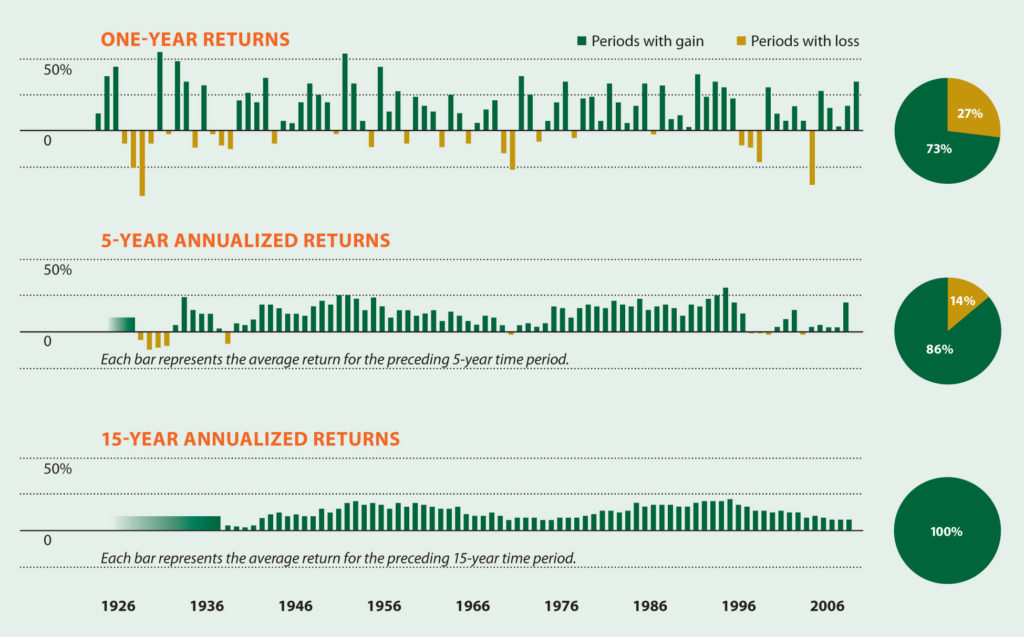

When it comes to investing, you simply can’t beat the market, and your financial advisor knows that.

We live in a world where the latest stock market news is available at your fingertips—whether that’s on a laptop in your living room or on a cell phone app that you can access while waiting for your order at the nearest lunch counter. Unfortunately, that means some may feel confident enough to make risky investment moves in an effort to outsmart the true formula for success: consistency.

Although it is possible for active managers to outperform the market (particularly in the short run), underperformance tends to be more probable after all fees and trading costs are considered. Consistent net outperformance is rare. This isn’t necessarily due to a lack of management skill; rather, it is a consequence of the burden of higher costs. Time is an important consideration in this relative performance comparison as advisors try to coach investors away from the distraction of changes in the short-term market conditions, whether positive or negative.

Financial planning

Often, people mistake investment management for financial planning. Financial planning is much broader, involving far more than the managing of investments. It involves:

- Asset and liabilities assessment

- Individualized cash flow analysis

- Retirement and Social Security planning

- Comprehensive risk management planning

- Tax efficiency planning

- Long-term investment and asset location strategy

- Crisis prevention and management.

For example, many clients assume that they must start Social Security benefits at retirement; but with strategic financial planning, your advisor can help you bridge the gap between retirement and age 70 in order to maximize your Social Security benefit.

A comprehensive financial plan put together by a trusted financial advisor can lead you to many planning opportunities, including Roth conversions, distribution planning, spending strategies for drawdowns, and limits on the amount of taxes you’ll pay.

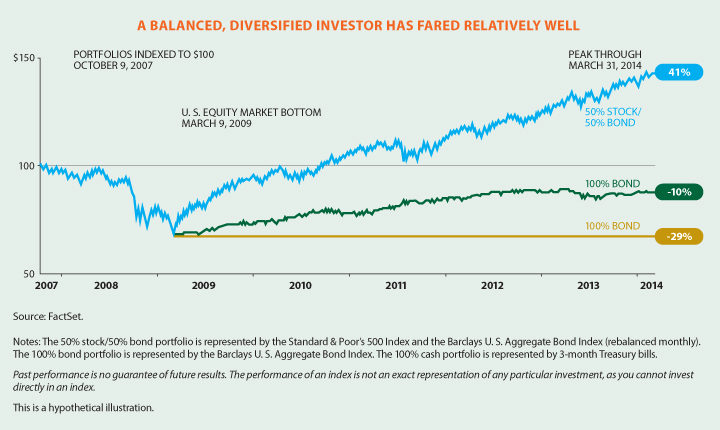

Managing expectations and behavior

Another significant value an advisor provides is behavioral coaching. The return on your investment in a financial advisor can be increased dramatically during market declines or rallies when you may be tempted to abandon your well-thought-out investment plan and move to cash. A good advisor will help you stick to your long-term financial plan during these tumultuous market swings.

Consider three hypothetical investors during the period between October 9, 2007, and March 31, 2014, each starting the period with a balanced $100,000 portfolio. The investor who moved this balance to cash at the 2009 stock market bottom lost $29,000. The investor who moved to an all-bond position at the stock market bottom lost $10,000. But the investor who stayed committed to the predetermined asset allocation, in the end, gained $41,000.

Asset allocation

Asset allocation

Providing a thoughtful investment strategy that manages risk with asset allocation is an important way in which advisors add value. For investors, risk tolerance is often closely associated with their goals—specifically the target retirement age and value of retirement accounts. Young investors without a fixed timeline have more flexibility to take risk, while investors closer to retirement tend to make decisions that leave less room for volatility. Time is truly the secret to making investments less risky.

At Cannon Financial Advisors, we believe primarily in the use of low cost, tax-efficient investments with an emphasis on index funds, which are a group of securities designed to replicate the performance of a broad market. Good asset allocation is crucial to matching one’s portfolio with one’s goals, needs, situations and risk parameters—all of which are subject to change.

Managing costs and fees

Another way your advisor can increase the return on your investment is by keeping your costs contained. That’s why Cannon operates on a transparent fee structure.

A good advisor also adds value to your overall investments by considering several tax angles. They find ways for you to maximize tax-favored accounts to delay the date at which taxes are due on those earnings. Since not all accounts are taxed the same way, good advisors identify creative solutions to reduce your tax burden. Finally, they can help you responsibly plan how to limit the impact of taxes on the income that your loved ones may receive following your death—making sure your financial legacy is as strong as it can be.

Several other tax angles your financial advisor may find that will help add value to your earnings include asset location, complex accumulation strategies, distribution planning and Roth IRA conversions. No matter the angle, your advisor can sit down with you and carefully discuss the best way to manage your costs and lessen the impact of fees—or avoid them altogether.

Portfolio rebalancing

Wealth management entails making regular changes to your portfolio to help maintain an acceptable level of risk, so that when you’re ready to withdraw, you can do so in a way that limits the taxes you’ll have to pay. A good advisor undertakes this complex task in a cost-effective and tax-efficient manner.

Rebalancing can also be used as a tool to reduce risk as clients near retirement age. It’s an effective way a good advisor can help you buy low and sell high without bringing market timing into the equation.

Diversity and security selection

Finally, a good advisor can help you make a wise asset class selection, ensuring clients have a diverse mix of asset classes that complement each other while also complementing a client’s overall risk tolerance. Adding in asset classes that have a low correlation to the stock and bond indices can reduce risk with little to no reduction in return potential.

While the extent of the value an advisor can add to your portfolio is based on your own unique situation and the way your assets are managed, it’s vital to understand that value goes far beyond security selection. Advisors have the ability to drive down both costs and risk while providing guidance, encouraging diversification and offering peace of mind.

In essence, your financial advisor is there to listen to you, counsel you and ultimately guide you on the right path, adding important value throughout the life span of your relationship.